What is Going on With Software? A Brief History of Public SaaS and the Current Crash in Stock Prices

- Kyle Johnston, CFA

- Feb 19

- 5 min read

Software stocks have collapsed over the last 12 months. Former darlings such as ServiceNow, Salesforce, Adobe, Atlassian, and HubSpot are down anywhere from 40% to 70%. This is type of price action is what happens when an industry goes from the stock market penthouse to the outhouse.

2015-2019: Growth in a Low-Growth Economy

Software-as-a-Service (SaaS) stocks were the kings of the post-GFC era. As cloud infrastructure and the SaaS model proliferated, revenue growth rates were high and persistent. Customers opted to move on-premise software into the cloud, reducing the time and money spent on maintaining software and hardware. Low interest rates and rising equity markets made capital cheap. Low economic growth led to tepid sales/earnings growth rates in many old-world sectors. The high and stable revenue growth of SaaS companies, along with strong balance sheets and minimal need for large investments in property/equipment, attracted flocks of investors. As revenues rose, valuation multiples (mostly tied to revenue rather than profits) expanded and annual returns over this period were incredible. SaaS quickly became the picture of predictable growth business models.

2020-2024: Work-From-Home, Rising Interest Rates, and the Emergence of AI

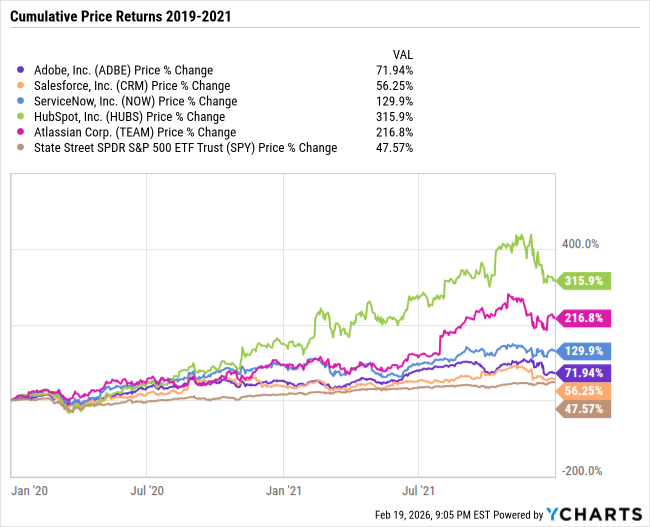

As the pandemic raged, the attractiveness of SaaS business models was amplified. While other areas of the economy crumpled, SaaS companies enabled the work-from-home phenomenon and kept businesses collaborative and productive. Businesses accelerated their purchases of cloud-based software driving higher sales growth at SaaS vendors. Again, high and stable revenue growth was rewarded by the market. Meanwhile, interest rates fell to zero and the cost of capital collapsed. A low cost of capital removes the friction of funding growth while rising share prices kept employees with stock compensation happy and feeling rewarded. At the same time, government stimulus flooded an economy stuck at home with little to spend on other than core goods. For many, rising cash balances found their way into a scorching hot stock market. SaaS shares rocketed higher and our sample group saw share prices increase anywhere from around 60% to over 300% between 12/31/2019 and 12/31/2021.

What followed this surge was 2022's violent collapse in share prices. Growth rates slowed, inflation rose, interest rates were rapidly hiked, and capital was no longer so costless. Our sample group saw max drawdowns of between 45% and 70% as valuation multiples compressed, equity risk repriced, and investors refocused their lens from revenue growth at any cost to profitable growth and improving margin trajectories. Companies often add stock-based compensation back to their announced earnings results because it is a cashless expense. While this may not be a cash expense, the bill eventually comes due in the form of investor dilution, which either slowly reduces the ownership stakes of existing investors or must be offset through stock buybacks from the companies’ cash on hand. Investors were happy to accept these adjusted earnings numbers when economic growth rates were low, interest rates were near 0%, and revenue growth was difficult to find. In 2022, revenue and earnings growth reemerged in other sectors as the economy emerged from the pandemic slumber. These adjusted earnings numbers were now more heavily scrutinized. SaaS was no longer the only game in town for sales growth and investors started to rethink the nosebleed valuations of the sector.

Inflation eased throughout the year, but the real spark plug that reversed the 2022 declines was the launch of ChatGPT. Investor enthusiasm returned to the technology sector and with it, a rising tide lifted all boats. From 11/30/2022 to 12/31/2024, share prices in our SaaS group rose between 29% and 155%. Software companies began to hint at ways they could deploy AI-based tools to their customers. Hopes for sustained growth, and maybe even reaccelerating growth, returned to investors' hearts. This excitement began to fade in 2025, ultimately kicking off the current downdraft.

2025-Now: Fears of Total Disruption

After bouncing sharply off the 2022 bottom, SaaS stocks began to slump in 2025. What began as disappointment in the rollout of AI related products transitioned to fear of disruption by the large language model platforms (ChatGPT and competitors) and AI-native disruptors. New tools such as Cursor and Claude Code showed incredible progress in the automation of software development. In addition, companies began to show success in AI implementations leading to reductions in employee counts in areas like customer service. In general, the current bear case for SaaS business models seems to be composed of the following: (1) automation through the use of AI agents and the resulting reduction in headcount needs at customers could pressure SaaS revenue that is based on the number of “seats” that pay to use the software, (2) the reduction in time and cost of software development could allow SaaS customers to build proprietary software and replace software purchased from third-party vendors, (3) cheaper software development could allow AI-native startups to rapidly gain share from larger competitors and/or could lead to pressure on the prices charged by incumbents, and (4) SaaS companies that pivot to a consumption-based model in which the customer pays for the use of computing resources rather than a fixed subscription fee could alter the economics and predictability of growth that once made SaaS companies king.

The way software stocks are trading would seem to show that most investors believe in some sort of combination of these risks. All of this boils down to a prime example of what can happen when an industry faces the risk of disruption. In Hemingway’s The Sun Also Rises, a character explains how he went bankrupt: “Two ways – Gradually, then suddenly”. The same answer could be used to describe how SaaS companies lost their premium multiple – gradually, then suddenly. When the narrative associated with an industry goes from “the most predictable growth in the market” to “possibly at risk of total disruption”, the associated stocks are in for a world of hurt.

Implications for Investors: Diversification Helps to Protect From the Unknown Risks

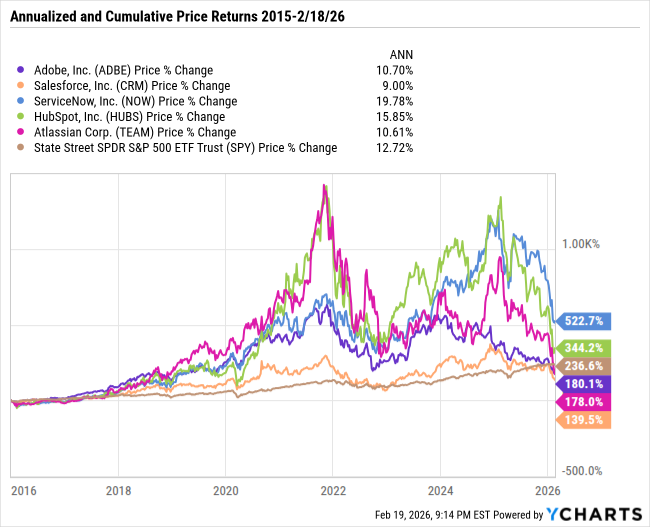

Markets often over extrapolate narratives in the short run as simple truths can lead to valuation re-ratings followed by momentum driven herd behavior and panic selling. The math of negative returns is brutal. A 60% decline in share prices can quickly wipe out much of your paper gains accumulated over a decade. The SaaS group used in this article had compound annual returns of between 17.6% and 32.3% from 12/31/15 to 12/31/24, with even the weakest returner handedly outperforming the S&P 500 return of 14.4%. Fast forward to present, and only ServiceNow and HubSpot are still outperforming the S&P since the end of 2015.

The current software sell-off could be a generational buying opportunity should these companies leverage AI tools to their advantage, using huge installed bases to distribute productivity enhancing solutions. On the other hand, this may be a true shift in the competitive landscape faced by a group of once dominant companies. The future is inherently uncertain. What we can say for sure is that this is another prime example of how quickly narratives can change and how swiftly disruption risk can arise in the ever shifting technology landscape. Two years ago, you would have been hard-pressed to find someone who was bearish on the future growth of the SaaS industry. This reinforces the principle that diversification not only helps protect investors from the known risks, but also from unknown risks. Additionally, diversification can help protect investors from behavioral errors driven by the core principal of prospect theory; that losses feel worse than gains. Most behavioral errors come during periods of enhanced volatility or dramatic drawdowns. Spreading your bets can help mute both of these, naturally reducing the emotional burden placed on the investor. For employees with large holdings in their company’s stock, the current landscape shows the importance of managing concentration risk. When diversifying feels the worst, it is often the most important time to do so.

Comments